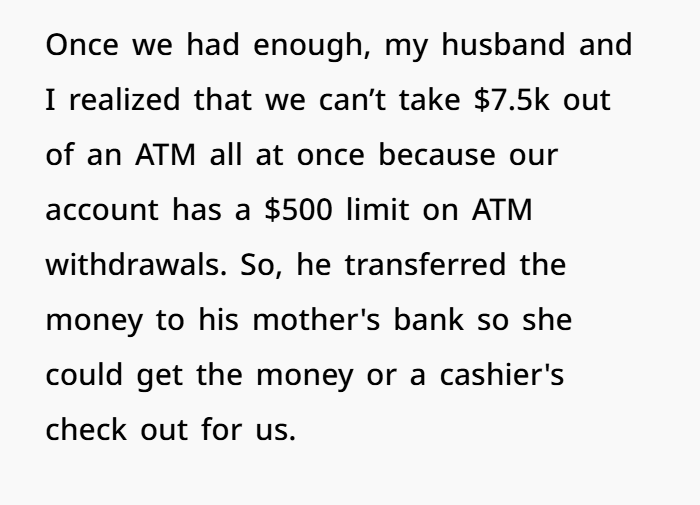

Husband Delays Wife’s Car Purchase — Secretly Loans the Money to His Mom Instead

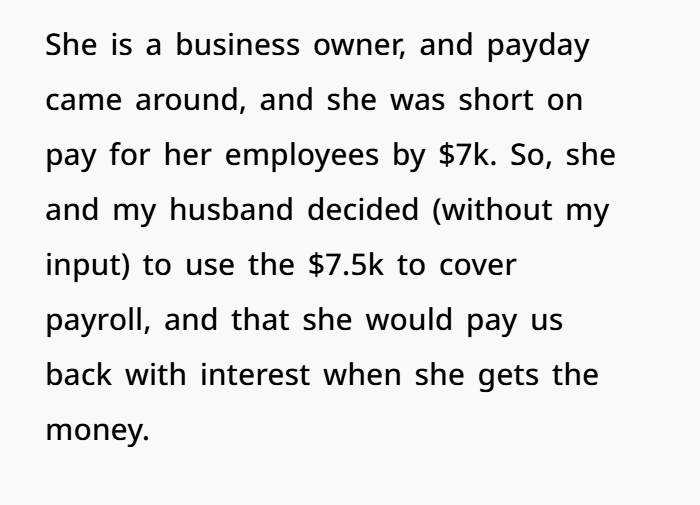

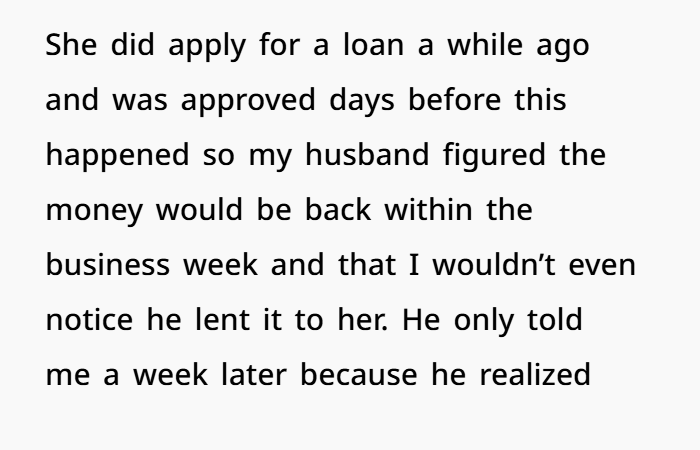

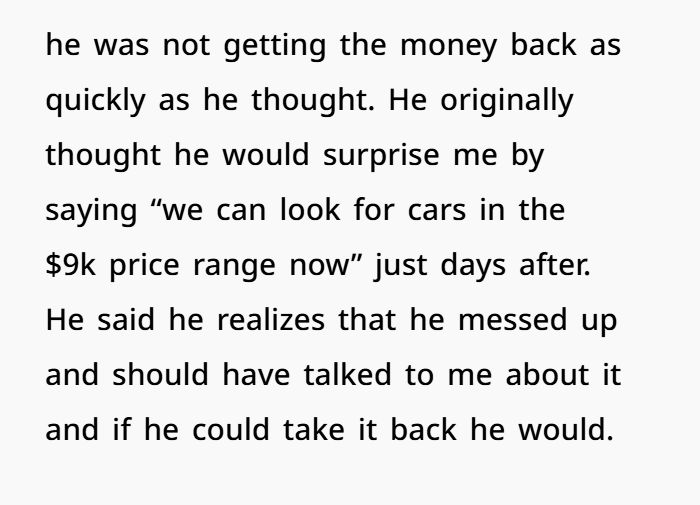

Trust and transparency are critical in any marriage, especially when it involves financial decisions that impact the entire family. In this situation, a stay-at-home mom and online college student found herself stranded without reliable transportation after a car accident totaled her primary vehicle. While she and her husband planned to replace the car once they had saved enough, a hidden decision derailed their plans. Without consulting his wife, the husband transferred their $7,500 savings to his mother’s business account to cover her payroll obligations, promising a quick repayment with interest.

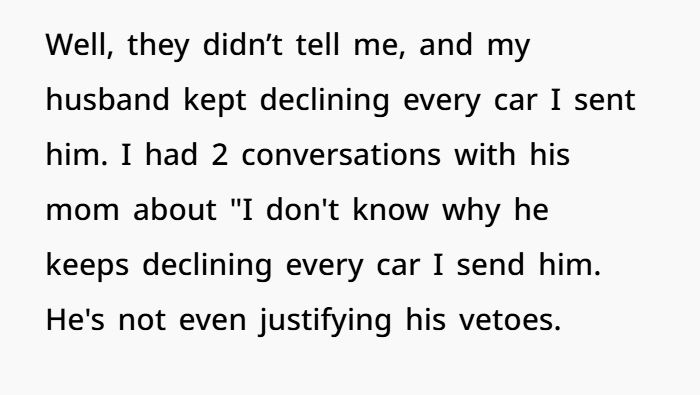

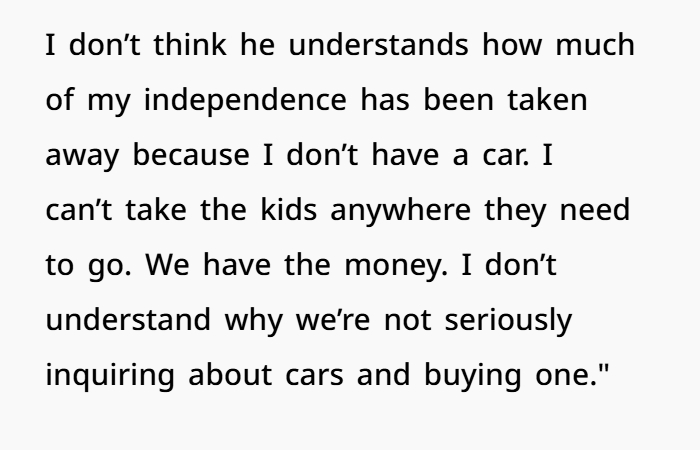

As days turned into weeks without the money being returned, the wife struggled with lost independence, caring for two toddlers without a dependable car. Feeling betrayed by both her husband and mother-in-law, the emotional strain deepened as new layers of deception came to light. Although the situation eventually resolved with full repayment and the purchase of a new vehicle, the breach of trust left lasting scars—highlighting the importance of joint financial decision-making and the risks of informal family loans.

Infidelity doesn’t have to be romantic to hurt, as this woman found out the hard way

After her car was totaled in an accident, she and her husband saved up $7.5K to buy a new one

At the heart of this story lies a classic example of financial infidelity, a term used to describe situations where one partner makes significant financial decisions without the other’s knowledge or consent. According to Forbes, financial infidelity affects nearly 30% of relationships and is a leading cause of marital strife, often ranking just behind issues like infidelity and addiction.

In this case, the husband’s unilateral choice to lend $7,500—critical emergency funds earmarked for a family necessity—exemplifies the dangers of informal loans to family members. Financial experts at NerdWallet warn that lending large sums to relatives, especially without a written agreement, is fraught with risk. Without legally binding contracts or clear repayment schedules, such transactions often jeopardize not only finances but also personal relationships.

Additionally, the practice of using personal savings to cover small business payroll is legally murky. According to Investopedia, small businesses must manage cash flow meticulously, and relying on personal loans from family members can create serious accounting and tax liabilities. If the mother-in-law’s business were to face legal challenges or audits, the lack of formal documentation could trigger compliance issues.

The wife’s sense of isolation and anger is deeply rooted in the loss of financial autonomy. Research by Pew Research Center shows that access to reliable transportation directly correlates with a parent’s ability to manage childcare, healthcare, and educational needs, making the deprivation of a car particularly burdensome for stay-at-home parents.

Furthermore, studies from Psychology Today emphasize that when financial infidelity is discovered, the damage to trust can mirror the emotional fallout of romantic cheating. Rebuilding that trust requires transparency, sincere apologies, and active steps toward shared financial planning.

Fortunately, the situation ultimately concluded with repayment and a new car purchase. However, the key takeaway remains stark: couples must establish firm financial boundaries, ensure mutual consent on large financial decisions, and treat informal loans to family members as serious, documented business transactions to protect both their marriage and their assets.

In the comments, readers agreed that the woman wasn’t overreacting, and one went so far as to say her mother-in-law can never be trusted with their money again